Do you think that the UK leaving the EU will not have a VAT impact on your business just because you aren’t VAT registered? Think again!

If you are not VAT registered the value of any services you buy from the EU count towards your turnover when determining if you need to register for UK VAT.

In some EU countries, there is no turnover threshold for VAT registration and so you may need to register for VAT overseas, even though you aren’t registered in the UK.

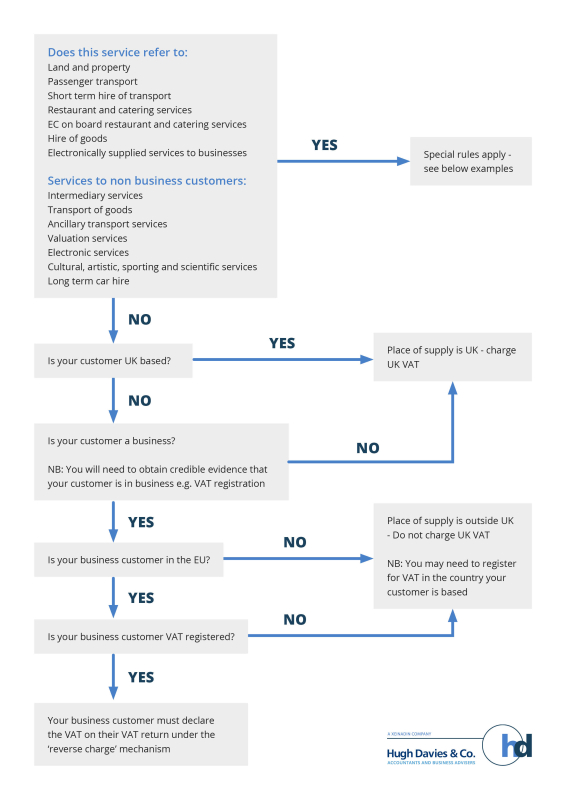

Whether you need to charge VAT or not will depend on where the place of supply of the service is deemed to have taken place.

Place of Supply General Rules

The UK’s general rules for the place of supply of services are that if the customer is not a business the supply is in the UK and so UK VAT must be charged. If the customer is a business, then the place of supply is where the customer is based, and no UK VAT is charged. However, things to consider don’t stop there.

We have simplified these rules on our handy flowchart.

Summary of some Exceptions to the Place of Supply Rules

Certain services relating to land are treated as made in the country in which the land is situated irrespective of where the supplier and customer are based.

Transport of passengers is treated as being made where the transport takes place. So, in some cases this will need to be in proportion to the distances covered in each country.

Hire of transport for periods of up to 30 days (90 days for vessels) is treated as made in the country where the transport is first made available to the customer, unless the services are effectively used in another country, the supply is then treated as made in that other country.

Supplies of restaurant and catering services are made in the place where they are physically carried out.

Hire of goods excluding transport is covered by the general rules unless the services are effectively used in another country, the supply is then treated as made in that other country.

Any service that is supplied to a business customer and effectively relies on the internet for its delivery is treated as supplied, for VAT purposes, where it is effectively used and enjoyed. For non-business customers it is treated as supplied where the customer belongs.

If you would like more information on how these rules may impact on you, please contact Hugh or Shirley on 01722 336647